FAQs

This page contains answers to commonly raised queries about development finance and the services offered by CPC.

This page contains answers to commonly raised queries about development finance and the services offered by CPC.

What is property finance?

Property finance in general terms is the ability for a purchaser to obtain a loan to assist in acquiring real property that is land, land and buildings, or home units provided such units are strata title. Traditionally finance is provided by banks via a mortgage document that is drawn up between a borrower and lender which is registered as a first ranking mortgage on the title deed.

What is property development finance?

Property development finance has shifted considerably post GFC from banks having market share to a significant reduction in their exposure to the sector. This is primarily due to regulatory pressures. APRA capital requirements imposed directly onto banks have led to reduced loan appetite in the commercial construction sector. This in turn has allowed non-bank lending to finance the property development sector. Non-bank lenders do not fall under the same APRA’s risk model requirements which allows them to offer more flexible finance solutions to developers.

How does development finance work?

Development finance can be sourced primarily from two sources – banks and credit unions (authorised deposit taking institutions- ADIs) or non-banks who are a wide range of lending institutions that do not hold a banking licence. Non-bank lenders are privately owned and rely on wholesale and sophisticated investors for their funding sources. The lender will usually rely on a specialist development finance broker to present the loan application as there are many factors for the lender to consider. These include the financial capacity of the developer (project sponsors) , project location, project mix and demand, profitability as well as the track record of the developer.

What are the different types of property development finance available?

Debt Finance – Commonly referred to as “senior debt” and provided by the lender either upfront (land purchase loan) or progressively (construction loan) at an agreed interest rate over a fixed period (usually 12-18 months). The debt is usually secured via mortgage document agreement that is drawn up between a borrower (developer) and lender (financier) which is registered as either a first ranking or second ranking mortgage on the title deed.

Equity Finance – These are funds provided to a developer (project sponsor) to assist with project costs. An equity finance position carries a greater level of risk as the return on equity (ROE) relies on the skill of the developer and market forces. Returns are generally in the form of a split of profit share that is agreed between the parties in the form of a shareholders agreement or Joint Venture (JV) agreement.

Preferred Equity Finance – Similar to debt finance but not as secure as any debt loan ranks ahead (1st or 2nd ranking mortgage on th title deed) in receipt of project proceeds at the end of a project. A preferred equity (PE) investment is usually in the form of a written agreement that outlines the terms of the investment. A pre agreed interest rate or coupon rate that provides a return between 18-25% on funds is common. The preferred equity initial investment and any agreed returns are paid out prior to the developer receiving their funds at the completion of a project and should reflect the risk profile and profitability of the project.

What is the best way to finance property?

This is dependent on many factors such as the location and demand for the property. Also key is if you are purchasing the property to live in (owner occupier) or as part of an investment (for either personal or business purposes). Once these factors are considered generally the financier (lender) will consider the merits of the property and look to understand if you have the ability to service and ultimately pay back the loan. The finance costs charged by the lender (fees and interest rates) will be reflective of this perceived risk profile.

Can you get 100% development finance?

Obtaining 100% finance of the project costs is possible only in circumstances where the developer has added substantial value via an uplift in the land value. This could occur where the developer has secured a site under option and obtained a DA for the highest and best use of the site. Some lenders will recognise this “sweat equity” and count this towards their financial contribution which may allow the developer to fund the agreed land purchase price and all development costs to complete the project.

Is CPC Development Solutions a lender?

No – we are a specialised development finance advisory that assist our developer clients to get their projects funded via top tier non – bank lenders.

What is your approach to getting projects funded, what value does CPC add?

We act for developers are not wedded to any particular lender. We like to get involved with our clients as early into the project as possible. We pull apart the developers feasibility and stress test all assumptions around revenue and cost and do a SWAT analysis of the project. This allows us to present projects to lenders professionally and honestly so they can assess risk and provide competitive pricing to reflect the risks.

Can developers approach these non-banks directly?

Absolutely but most non-bank lenders prefer to deal with introducers like CPC. We advise if there is already a strong existing relationships with a lender then deal direct but we always look to introduce developers to new lenders who they might not have come across in the marketplace. We negotiate on behalf of the developer get the best deal terms. We sell the sponsors ability to deliver a quality product and put up a case as to why this project is a great funding opportunity for the lender. Our relationships with lenders are the key to our success – when we bring a project to a lender they know its been vetted and worth funding!

Why is development finance important?

Successful developers look to conserve capital where possible and achieve a business model that allows them to better manage their exposures and cashflow. They do this by setting up projects at different stages of the development cycle and obtaining finance in various forms to suit each project. Development finance can be in the form of senior debt, mezzanine (junior) debt, equity (JV or preferred). Having a balanced approach with reliable lending channels will ensure survival over project cycles and also allow recurring cashflow to sustain the business.

How does CPC ensure your lenders provide market leading rates?

Within our network of non-banks we communicate with them frequently, we understand their risk appetite and their areas of operation. This all effects their rates (which change frequently depending on their funds at hand and projected inflows). We get complete market coverage within our network in a discrete and competitive way that ensures the deal doesn’t become stale or over shopped in the marketplace. We match our developers with the most suitable lender – this will always be reflected in the strength of the deal.

What is the smallest loan size your lenders consider? Do they provide renovation finance?

$2m – Our lenders only deal with commercial transactions (GST registered ABN businesses). We don’t look to fund mum and dad type loans or renovations – they are best left to the major banks.

How hard is it to get a commercial loan?

Obtaining a commercial loan is fairly straightforward with the right business plan. The quality of your loan application is of high importance as you want the lender to fund your project (not someone else’s). A lender will usually rely on a specialist development finance broker to present a project and will include the financial capacity of the developer (project sponsors) , project location, project mix and demand, profitability as well as the track record of the developer.

How much do you have to put down on a commercial loan?

The amount of equity required is dependent on several factors including where the project is placed with development approvals, the purchase price of the site, total development costs and overall projected profit margins. Generally speaking the banks will require a higher amount of cash from the developer that a non-bank. The key metric lenders will assess is the Loan to Value Ratio (LVR).

What is the typical length of a commercial loan?

A typical commercial loan for construction projects would be for 12-18 months. The loan is usually repaid at the end of tis term from each of the purchasers taking ownership of their completed house, apartment or commercial property.

What type of security is required?

The following is generally required:

Are the rates, fees and charges negotiable?

Yes – Non- bank lenders can be more flexible than the banks. Well located projects with relatively low risk profiles will result in sharp pricing and a willingness from the lender to negotiate.

What are the pitfalls of non-bank lending?

There are many. Low balling of interest rates, high fees, long minimum interest periods, brokers who front as lenders, punitive penalty clauses – these should all be red flags. It’s a totally unregulated sector with a reputation for unscrupulous operators. Lenders that have a good track record for showing flexibility and are solutions focused when things don’t go to plan is what to look for (resolving COVID construction delays are a good example).

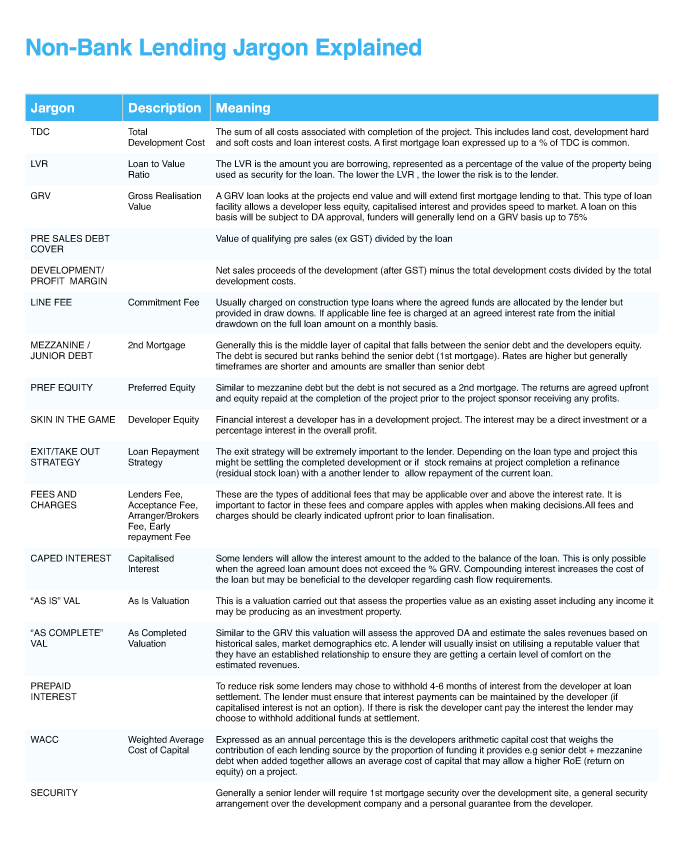

There is a lot of jargon and abbreviations used in the non-bank sector. What does it all mean?

We have pulled together a cheat sheet:

If I want to get some indicative feedback on my project what’s the next steps?

You can start by either filling in our short 5min project information form on the Get Started page.

Alternatively you can contact us on m. +61 0434 932 634

Crowd Property Capital Pty Ltd (CPC)

A registered company under the Corporations Act 2001, ACN 600 539 544

An accredited member of the Finance Brokers Association of Australia (FBAA) Member No M-352808

![]()

A licensed Corporation under the Property, Stock and Business Act 2002, Corporation License No. 10065109.

A member of the Real Estate Institute of NSW (REINSW)

David Lovato (Sole Director) holds a Certificate IV in Finance and Mortgage Broking and Property Services (Real Estate Agents License No 201 604 57 )