The New South Wales government’s 2025–26 state budget has given a significant boost to residential property development by announcing a $1 billion Pre-Sale Finance Guarantee scheme.

This initiative aims to unlock stalled housing projects across the state by helping developers secure finance earlier, speeding up construction and increasing housing supply.

Financing bottleneck

This scheme, an Australian first, addresses a critical bottleneck that has plagued developers: the strict pre-sale requirements imposed by traditional lenders.

Traditionally, banks and lenders require developers to pre-sell between 50% and 80% of dwellings in a project to qualify for loans. This high pre-sale threshold has been a major hurdle, particularly for medium-density developments and apartment projects, often causing delays or indefinite stalling of many approved housing developments.

In fact, recent research by SuburbTrends, commissioned by MCG Quantity Surveyors, revealed that one in six approved unit projects around the country fail to get built. This results in “phantom towers”– approved projects that remain unbuilt for years, contributing to the state’s housing shortage.

The new Pre-Sale Finance Guarantee scheme aims to tackle this obstacle between approvals and construction.

How the scheme will work

Developers who have secured planning approval and have lender terms that require pre-sales to commence construction, can apply for the guarantee.

In it, the government will act as guarantor for up to 50% of eligible off-the-plan housing projects, providing between $5 million and $50 million per development.

Once approved, construction must begin within six months. If the project’s dwellings sell out as planned, the government’s guarantee is dissolved, and the funds are recycled back into the scheme for other projects.

But if homes are not sold, the developer can call on the guarantee, selling the unsold homes to the government at a discounted rate (at a minimum of 10% of the market value). The government can then sell, rent or convert them into affordable or social housing, ensuring that some form of housing supply is delivered regardless.

To qualify for the program, developers will need to undergo the state government’s credit assessment process. This will take into account the merits of the project and the capacity, capability and credibility of the developer and their delivery team.

Developers will pay an application fee to have your project assessed. If successful, you will also be charged a line fee for the duration of the government’s financial exposure.

This line fee is similar to the interest you’d pay on a loan facility. It’s calculated as a percentage of the amount the government is guaranteeing and reflects the cost of having that financial backing in place. The exact rate will be pre-determined and applied annually until the guarantee is extinguished.

The scheme is expected to come online later this year, with initial applications anticipated to be accepted from October 2025.

The fund will support up to 5,000 apartments, which is projected to unlock the construction of 15,000 new homes over the next five years.

Other budget announcements

In addition to the Pre-Sale Finance Guarantee scheme, the NSW government announced several other initiatives aimed at improving housing supply:

Permanent build-to-rent tax concession: A 50% reduction in land value for eligible projects will now apply indefinitely, encouraging more high-quality rental developments. This concession was previously due to end in 2039.

Works-in-Kind credit: An offset will be available for approved infrastructure costs, such as roads or land for schools, against the Housing and Productivity Contribution.

$145.1 million for Building Commission NSW: A funding boost will support stronger regulation, more inspections and improved construction quality.

$3.4 billion skills investment: This investment will train over 23,000 new construction apprentices and offer up to 90,000 fee-free training places.

$122 million to streamline planning approvals: This aims to increase planning resources, support infrastructure delivery and accelerate housing approvals.

CPC Lending Solutions is a property development and residential finance specialist. Whether you’re a developer needing funding for land, construction, or residual stock, or a buyer looking for the right mortgage, we’re here to help. Contact us at info@crowdpropertycapital.com.au or fill in this form.

When applying for development finance, understanding how lenders assess risk can significantly improve your chances of approval. Beyond the numbers, they evaluate the project’s viability, your experience and the safeguards in place if things don’t go as planned.

Here are five core considerations:

1. What level of security can the borrower offer?

Security gives lenders protection if the loan isn’t repaid. In development finance, this usually includes:

First mortgage over the site – This is the main form of security, giving the lender the right to sell the land if the loan defaults.

General Security Agreement (GSA) – Covers broader business assets like equipment, IP, and income rights.

Directors’ personal guarantees – Adds extra assurance by making you personally liable if the company defaults.

The stronger the security, the more favourable your funding terms are likely to be.

2. What experience does the borrower and project team have?

Lenders prefer borrowers with a proven track record. They’ll assess your past projects and your team’s experience, including the builder, project manager, and consultants. A capable, experienced team gives lenders confidence that the project will be delivered on time and within budget.

3. What level of funding is required?

Be clear about how much funding you need and how it compares to the project’s value and cost. Lenders look at:

Loan-to-Value Ratio (LVR)

Loan-to-Cost Ratio (LCR)

Lower ratios mean lower risk, which can lead to better terms. Having your own equity invested is also viewed favourably.

4. Is the project profitable?

Lenders want to see that the project has a healthy profit margin. A well-prepared feasibility, supported by budgets, timelines and market data, helps build confidence. Pre-sales can further strengthen your case by showing demand and providing a clearer loan repayment pathway.

5. Are there contingencies and an exit strategy in place?

Lenders want to know you’ve accounted for risks like delays, cost overruns, and planning issues. A clear exit strategy – whether through pre-sales, asset sales, or refinancing – is essential. Strong risk management and a defined loan repayment plan go a long way in securing approval.

Need expert guidance? CPC Lending Solutions specialises in development finance for land, construction, and residual stock. We help structure your application and connect you with the right lender. Email us at info@crowdpropertycapital.com.au or contact us here.

https://crowdpropertycapital.com.au/wp-content/uploads/2025/07/What-type-of-security-is-required-for-construction-finance.jpg10801620dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2025-07-10 08:46:202025-07-10 08:46:205 key lender considerations when seeking development finance

With the election now behind us and interest rates set to fall in the coming months, lenders are adjusting their criteria to win new business in the housing sector.

The re-elected Labor Party has some ambitious plans for the country’s housing and construction sectors. It is a multipronged approach that aims to assist the demand for housing from the supply side (developers have more certainty in their end buyers), as well as allowing consumers into their homes faster (particularly first home buyers) by lowering entry barriers to property ownership.

These policy changes are significant for property industry professionals and borrowers alike, as they will have a profound impact on the housing market.

What you need to know about the new federal Labour policy settings

1. Boosting homeownership for first home buyers

Labor has pledged $10 billion to construct 100,000 new homes over eight years, specifically for first home buyers, reducing competition from investors.

From 2026, the government will remove income limits for the First Home Buyers Guarantee, allowing all first home buyers to purchase a home with a 5% deposit without needing lender’s mortgage insurance (LMI).

Additionally, the Help to Buy shared equity scheme will expand, letting the government cover up to 40% of a home’s purchase price.

Lenders will target first home buyers and offer extremely competitive loans, they will want to get market share as the government policies will fuel loan security and longer-term capital growth.

Developers that provide exclusive new housing stock will qualify for construction funding with lower hurdles around required developer equity and presales.

2. Addressing the tight rental market

Labor’s Build to Rent (BTR) scheme includes tax incentives for developers who deliver BTR apartments with a portion of units set aside at below-market rents.

Developers will be encouraged to take on smaller BTR projects in established areas and provide more housing where needed. These include projects like new age boarding houses, short-term accommodation and larger BTR development.

3. Tackling housing supply constraints

Labor’s broader housing strategy includes a $78 million investment to fast-track the qualification of 6,000 apprentices, $54 million for prefabricated and modular home manufacturing, and $120 million to incentivise states to remove red tape around housing approvals.

Developers are already seeing an easing of construction costs through a combination of factors, for example, material cost decreases, off-site manufacturing, efficiency in site programs and stabilisation of wage growth.

Red tape around dwelling approvals and construction certificate approvals is starting to be cut as the industry gets to a better equilibrium between authority/approval costs, quality of construction and weeding out from the industry the dodgy developers and builders.

The government has tightened its already restrictive policies around foreign ownership. This move around new product restrictions will be further welcomed by locals getting frustrated by missing out on home ownership.

5. Focusing on social housing

The government aims to deliver 55,000 social and affordable homes through the Housing Australia Future Fund and has allocated $1.2 billion for new crisis and transitional housing for vulnerable groups, including older women, young Australians, and those escaping family violence.

For developers in this space, this initiative will be a big driver of project starts. There are numerous state grants also available for affordable housing as governments try to do more to assist vulnerable people in a competitive housing market.

What is the expected impact on the market?

The overall impact is one of growth. These policy settings will increase activity in the property sector. Combined with lower interest rates moving into 2026, we will see more developers bringing projects to market and more homeowners and investors getting back into the property market.

CPC Lending Solutions is a property development and residential finance specialist. Whether you’re a developer needing funding for land, construction, or residual stock, or a buyer looking for the right mortgage, we’re here to help. Contact us at info@crowdpropertycapital.com.au or fill in this form.

https://crowdpropertycapital.com.au/wp-content/uploads/2025/05/Mays-image.jpg8941280dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2025-05-15 11:45:032025-05-16 07:48:53What you need to know about the new federal Labour government’s housing industry policies

Property development can often be complex as it encompasses everything from land acquisition to construction and fitout.

To ensure that property development projects can be completed and potentially turn a profit, understanding the different financing options is key. By delving beyond means of senior debt, developers can access another level of funding that could prove beneficial both now and in the future.

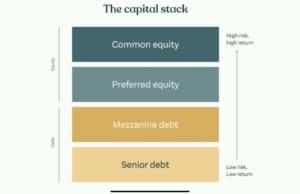

Taking up their own space in the capital stack are the opportunities of mezzanine financing and preferred equity financing. Understanding the subtleties between these financing options helps developers answer the common question: “which option is more suitable for my project?”.

What is Mezzanine Financing?

Mezzanine financing is essentially a hybrid of debt and equity that sits between senior debt and common equity in the capital stack. As such, it is often viewed as an option for developers who are looking to bridge a funding gap.

To understand the intricacies of mezzanine financing and how it might be applicable to a property development project, it’s essential to also acknowledge common terms such as senior debt and capital stack.

As such, senior debt is defined as borrowed money that a company must repay first. As this type of debt has the highest priority, it bears the lowest risk which, in turn, results in lower interest rates. The most common type of senior debt is from financing institutions like banks.

In relation to the capital stack, this is a term used to refer to the layers of capital that have gone into a project. The capital stack highlights who will receive funds or profits and in what order this will take place.

With this in mind, mezzanine financing is often referred to as the middle layer in the capital stack as it falls between senior debt and any equity. As the debt is secured and falls in this middle layer, such a loan will carry a higher risk profile, resulting in higher interest rates.

Despite the associated higher interest rates and the potential of lenders imposing stricter borrowing conditions, mezzanine financing is a viable and common option for property development projects. Especially when you consider that it is non-dilutive.

What is Preferred Equity Financing?

Preferred equity is another common financing option utilised by property developers. Preferred equity financing involves the developer giving the lender a stake in the project. In relation to the capital stack, preferred equity sits above common equity but below debts such as mezzanine.

With this positioning in the capital stack, the provider of preferred equity financing will receive profits and have their debts repaid before common equity stakeholders such as the developer themselves.

This level of ownership also affords the lender or the investor with the ability to be involved in a decision making level. There is also the ability to take control of the project if things are not following the outlined plan.

Key Differences Between Mezzanine and Preferred Equity?

Where mezzanine financing is viewed as bridging the funding gap, preferred equity is seen as sharing the risk and reward of a project. As such, there are many key differences between mezzanine and preferred equity financing for property development funding.

Mezzanine Financing

Preferred Equity

Risk Profile

As the middle layer in the capital stack, mezzanine funding falls between senior debt and equity. While the risk profile is high, mezzanine has a higher claim on assets than preferred equity.

Its position in the capital stack means that preferred equity is subordinate. Therefore the risk profile is higher than debt but lower than common equity.

Control Rights

Mezzanine lenders do not get involved with the progression of the property development project.

Preferred equity investors may negotiate voting rights and therefore have a say in how the project progresses.

Return Structures

Mezzanine loans require interest payments and due to the risk profile, the interest rates are higher than those associated with senior debt.

Preferred equity investors will receive a fixed return or dividend based on their stake in their project.

Collateral Requirements

As a second ranking mortgage a mezzanine loan is secured.

Preferred equity, unlike debt, is typically not secured. However, returns are secured through the lender or investors stake in the project.

Where mezzanine financing is viewed as bridging the funding gap, preferred equity is seen as sharing the risk and reward of a project. As such, there are many key differences between mezzanine and preferred equity financing for property development funding.

Benefits and Drawbacks of Each Financing Option

As financing options for property development both mezzanine and preferred equity financing have positive and negative aspects that need to be considered. Understanding the intricacies of both will help developers choose the right method of alternative financing for their specific project.

Mezzanine Financing

One of the main benefits of mezzanine financing is the ability to secure funding without having to dilute the share of equity. Additionally, as this method of financing acts as a second mortgage of sorts, there are fixed repayment terms. This helps to provide predictability which plays a large role in having the money set aside to make the payments. It is also worth noting that interest payments may be deducted as an expense, making them tax deductible.

With mezzanine financing there are also negatives to consider, namely, the fact that due to the increased risk, interest rates will be higher. This leads into another negative as with mezzanine financing there is a larger risk involved because of the increased debt and interest obligations. As a secured form of financing, mezzanine lenders have the right to collateral in the case of default which can lead to foreclosure.

Preferred Equity Financing

Preferred equity financing can be a viable option for property developers looking to finance their latest project without increasing debt ratios. For example, this type of financing can be structured flexibly so that investors do not receive additional profits if returns outperform expectations. It’s also worth noting that mandatory interest payments can be deferred during the construction phase to help developers increase cash flow at such a pivotal point in the project.

When opting for preferred equity financing, developers sacrifice both profit and control. With preferred equity, investors will also receive higher returns when compared to mezzanine financing. With preferred equity investors receiving a portion of the profits, developers have to share the reward of their hard work. It’s important to highlight that if preferred equity investors have negotiated voting rights, they can also influence how a project progresses.

When to Choose Mezzanine vs Preferred Equity

When choosing between mezzanine and preferred equity financing it’s important to approach the decision with an outcome in mind. If you’re looking for a tool by which to bridge a gap in funding, mezzanine will be the most obvious choice. For those wanting to share both the risks and rewards of the project with another party, preferred equity is advisable.

The right choice will be dependent upon a variety of different factors as well as project specific features. This is why the risk appetite of the developer and the project’s overall financial profile heavily influence the final decision.

There are situations where one alternative is more suitable than the other. As an example, a project where cash flow is limited may find financing a mezzanine debt difficult. Therefore, rather than going into more debt, the developer leverages preferred equity’s profit participation to access the funds needed to complete the project.

As another example, consider a developer with stable cash flow projections looking to help secure the extra funds needed to help complete a portion of the project that has yet to sell off the plan. Rather than giving up profit participation in the overall project, choosing mezzanine financing means maximising leverage today without diluting ownership tomorrow.

CPC’s Role in Property Development Financing

As a fully independent finance brokerage, CPC Lending Solutions works with developers to find solutions tailored to suit both financial circumstances and the overall goal of the project. All of which lays the foundation needed to structure the right funding mix.

By offering tailored services, CPC Lending Solutions investigates different funding models so that the final outcome – be it undertaking a mezzanine loan, preferred equity financing or a hybrid funding model – is the most suitable for your personal and professional needs.

Development and construction financing models can be complex, however, this highly specialised area of financing is a key skill of CPC Lending Solutions. Our expertise works as a key asset for developers looking to capital stacks to help optimise project returns.

Choosing the Right Financing for Your Project

Funding a property development project can be a complex endeavour. In order to achieve the best outcome possible, developers may need to look at the different layers of the capital stack. In property development financing, key components of the capital stack are mezzanine and preferred equity financing.

While both provide funds to property developers, each financing option has unique characteristics. To choose between taking on a mezzanine loan, which is also referred to as another layer of debt, versus preferred equity financing, where part of the exchange involves sharing control and profits, developers need the right guidance.

CPC Lending Solutions have the experience and expertise to help structure the most suitable financing package for your project, no matter how complex the capital stack may seem. Contact David Lovato on 0434 932 634 or email dlovato@crowdpropertycapital.com.au to explore flexible funding options for your next development project.

https://crowdpropertycapital.com.au/wp-content/uploads/2025/04/thumbnail_image0.jpg12421920dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2025-04-13 06:10:482025-04-29 10:20:07Understanding financing options in property development

If you work in property development, you’ve probably heard rumblings about iCIRT. But what is it – and why does it matter?

In short, iCIRT is an independent, data-driven star-rating system designed to give developers, builders, financiers, insurers and – soon – consumers more confidence in the building industry. It helps identify trustworthy professionals and weed out risky players – making it easier to choose the right people for your projects.

For developers, iCIRT has the potential to be a game-changer – not just for project delivery, but also for financing, insurance and competitive positioning.

What is iCIRT?

iCIRT stands for the Independent Construction Industry Rating Tool. It was developed by Equifax (the credit rating agency) in partnership with government and industry, in response to a clear need for greater trust and transparency in the construction sector.

Each iCIRT rating assesses a business or professional’s ability to deliver safe, compliant, and durable Class 2 buildings (i.e. apartments, townhouses and other multi-unit dwellings). The result is a star-rating from 0 to 5, with 3 gold stars or more indicating a trustworthy operator.

Unlike traditional credit ratings, iCIRT doesn’t just look at the numbers. It pulls in thousands of data points – both public and private – to assess six key areas:

Capability

Conduct

Character

Capacity

Capital

Counterparties

The result is an objective, independent snapshot of a building professional’s trustworthiness, risk level and track record.

Why does iCIRT matter to developers?

In recent years, the development sector has been under scrutiny. High-profile building defects, regulatory changes and increasing consumer scepticism have put pressure on everyone in the supply chain to lift their game.

That’s where iCIRT comes in. It gives developers a practical way to identify reliable consultants, builders and subcontractors – and prove their own credibility too.

Here’s why that matters:

Better project teams – Use iCIRT reports to assess the professionals you bring onto your projects. You’ll reduce risk, improve quality and be more confident in your delivery partners.

Increased consumer trust – As iCIRT becomes more visible to buyers, being associated with iCIRT-rated professionals (or having your own rating) could become a powerful trust signal.

Easier access to insurance – An iCIRT rating can help you qualify for 10-year insurance on your developments, reducing friction with buyers and financiers alike.

Stronger market positioning – A high iCIRT rating sets you apart from the pack. It shows you’re proactive, transparent and serious about quality – all of which can give you an edge in a crowded market.

How to use iCIRT to your advantage

There are two main ways developers can engage with iCIRT:

Order a report on your project team – If you’re engaging a builder, consultant or supplier, you can request their iCIRT star-rating and report. This helps you assess their credibility before bringing them on board.

Get your own iCIRT rating – You can self-rate your development business through Equifax. It involves a detailed assessment of your history, practices, finances, project delivery and more. The process typically takes 5-10 days and costs between $1,750 and $9,950 (ex-GST), depending on the depth of the report.

Once rated, you’ll receive a detailed report showing how your business compares to others in the industry – including your star-rating, key strengths and areas for improvement.

The bottom line

iCIRT is more than just another compliance tick-box – it’s a tool that smart developers can use to build better, earn trust and compete more effectively.

Whether you’re a large-scale developer or a boutique builder, now’s the time to consider how iCIRT fits into your risk management, procurement and branding strategies. In an industry where trust is everything, a little star power could go a long way.

As adoption grows, iCIRT may well become an industry standard – so getting ahead now could pay off later.

CPC Lending Solutions is a property development and residential finance specialist. Whether you’re a developer needing funding for land, construction, or residual stock, or a buyer looking for the perfect mortgage, we’re here to help. Contact us at info@crowdpropertycapital.com.au or fill in this form.

https://crowdpropertycapital.com.au/wp-content/uploads/2025/04/iCIRT.jpg8471280dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2025-03-10 03:51:382025-04-29 10:22:23Why iCIRT is set to transform the property development industry

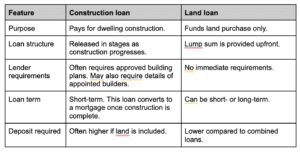

When planning to build a new home, a common question asked by borrowers is “Does a construction loan include land?”. Understanding this and how a construction loan works can impact your financial strategy.

A construction loan is a type of short-term financing designed to cover the cost of building a new dwelling or substantially renovating an existing one. Unlike a conventional mortgage, which provides a lump sum upfront for the purchase of an existing property, a construction loan is paid out in stages as your building project progresses. This is also known as ‘drawing down’ your funds.

One of the key differences between a construction loan and a regular mortgage is that you will only pay interest on the amount drawn down in your construction loan. This can help keep your monthly repayments lower.

It is a common assumption in property development financing that construction loans automatically include the cost of the land, too.

Does a construction loan cover land?

Whether or not a construction loan covers land depends on the lender.

Some lenders allow borrowers to bundle the purchase of land with the construction of the dwelling into one home loan. This single loan covers both land acquisition and construction. The loan will be disbursed in stages, with the first release of funds used to purchase the land. Thereafter, the loan functions as a construction loan, paying out in stages as your build progresses.

But, other lenders do not offer a bundled loan, instead allowing separate financing. This might require you to take out a land loan first and then apply for a construction loan once the building plans have been finalised.

From a lender’s perspective, these two options cover a range of scenarios, including developers or borrowers who already own the land and now just require financing to build the dwelling.

Additionally, for landowners who have low or no debt on their land, some lenders may offer an equity release option. This allows the landowner to access the equity in their land as part of the construction loan, providing additional funds for the project or even for securing their next development.

In certain scenarios, the lender may provide a cash-out component at the start of construction, allowing developers to secure their next project while the current one is being built. This will depend on maintaining the overall construction maximum loan-to-value ratio (LVR), but it can be particularly helpful for developers managing overlapping projects.

However, this process varies from lender to lender, so it’s recommended you work with an experienced finance broker who can help you find a loan that suits your current financial situation and long-term goals.

At CPC, we understand that every project is unique. Our approach to property development financing is to work closely with borrowers to understand their specific circumstances and tailor a financing solution that meets their individual needs. We consider the project as a whole, including the land acquisition if necessary, to find a financing solution that works for you.

Key factors that determine construction loan structure

Lenders will assess several criteria when deciding whether a construction loan can include the land purchase. These may include:

LVR: This represents the percentage of the total project cost (including land) covered by the loan amount. A lower LVR means you will need a larger deposit.

Borrower’s deposit: If you want to include the purchase of the land in your construction loan, you may need a larger deposit.

Construction timeline: Some lenders require construction to commence within a set period after the land purchase. This ensures that the land is used as intended and that the project progresses as stated in the plans.

Land zoning and permits: Lenders often require approved building plans and necessary permits before approving land financing to reduce the risk of project delays or complications.

Construction loan versus land loan: What’s the difference?

If a bundled loan is not an option for you, or there are other reasons you want to separate the two, it is helpful to know what the differences are between a construction and land loan.

Land loan: This is typically used to purchase vacant land without immediate plans for construction. This type of loan often has shorter terms and higher interest rates than construction loans

Construction loan: This will finance the building of the dwelling and is drawn down in stages. Borrowers will likely be required to provide approved plans to the lender.

How CPC helps borrowers finance land and construction

At CPC Lending Solutions, we understand that every borrower’s situation is different. Whether you need a construction loan for land and building, a separate land loan, or alternative financing options, we can help find a solution that aligns with your property development goals.

Our expertise is in property development financing, which allows us to find flexible and tailored loans for your project’s needs. Working with a specialised lender like CPC Lending Solutions means you have access to more knowledge of the industry as well as personalised service.

If you’re exploring how to finance land and construction, our team at CPC can guide you through the process. Contact CPC Lending Solutions today to discuss your construction and land financing needs.

https://crowdpropertycapital.com.au/wp-content/uploads/2025/02/Does-a-construction-loan-include-land.jpg10801920dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2025-02-26 09:15:342025-02-26 09:15:34Does a construction loan include land?

When it comes to property development, finding a lender that can keep pace with the unique demands of each project is crucial. Finding one with a deep understanding of the industry is just as important.

That’s why we started this series: to highlight lenders who offer innovative loan solutions for property developers

Dorado – a lender with a strong reputation for flexibility, speed and creativity – has established itself as a standout for developers, funding over 256 deals across Australia over the past 15 years.

What sets them apart?

Dorado’s key difference is its ability to provide tailored financing solutions that go beyond the usual metrics like loan-to-value ratios. Unlike traditional lenders who rely on strict lending criteria, Dorado takes a more holistic view. Each project is assessed based on its unique needs and market conditions, allowing Dorado to offer adaptable loan solutions that address specific challenges.

A strong focus on property development

Dorado has a large and growing interest in financing property developments throughout Australia. They actively support a broad spectrum of projects, including residential, mixed-use, commercial and industrial properties.

Their funding approach is focused on quality and viability. Dorado looks for developments with a clear, achievable path to completion, ensuring they back projects that deliver measurable results. By offering both first mortgage and subordinate finance solutions, Dorado provides developers with the capital they need to bring their visions to life.

Unique features and policies for property developers

Dorado offers several unique features designed to benefit property developers. Their funding options include solutions such as first mortgages, mezzanine debt, preference equity and direct investments. This variety allows them to customise solutions to suit specific project requirements, providing developers with the financial agility they need.

Alongside these funding options, Dorado has streamlined its processes to ensure applications are quickly assessed, which is a major benefit for developers where timing can often be the difference between success and a missed opportunity.

Why developers choose Dorado

Three key reasons stand out:

First, Dorado offers invaluable industry expertise. Their team has extensive experience in property development financing and an understanding of the industry and market. This translates into practical insights and guidance that developers can use throughout their projects.

Second, Dorado provides personalised support and prioritises building strong client relationships. They take the time to truly understand a developer’s needs and offer tailored support. By personalising the experience, Dorado becomes a partner in the process rather than just a lender.

Finally, Dorado puts transparency and communication at the centre of its work. Its emphasis on consistent, long-term partnerships means developers have come to rely on Dorado as a lender they can trust.

Dorado is a lender that meets the needs of many developers, but they might not be the perfect fit for everyone. That’s where CPC Lending Solutions comes in. We work with lenders like Dorado to connect you with the best financing solution for your project. Whether you’re tackling a residential build or a large-scale mixed-use development, we’re here to help.

The Australian housing market has seen a growing divergence in the value of new builds compared to older homes. This trend has been influenced by factors like energy efficiency, maintenance costs and changing buyer preferences.

Energy efficiency and minimum standards

Under the Nationwide House Energy Rating Scheme (NatHERS), the National Construction Code (NCC) introduced a minimum 6-star rating (out of 10) for new builds from 2010 and adjusted the mandate recently to a minimum of seven stars.

These standards ensure that newly built homes automatically include superior insulation, efficient heating and cooling systems, and measures to reduce dampness and mould and improve overall comfort.

In its December 2024 report “Amped up: How energy resilient are Australian homes?”, CoreLogic noted that a typical home built in 2010 or later achieves a median star rating of 5.9 out of 10, compared to just 2.8 stars for homes built earlier.

This disparity places older homes at a disadvantage, particularly for environmentally conscious buyers or renters.

Growing buyer and investor demand for energy efficiency

Savvy buyers, both owner-occupiers and investors, are increasingly willing to pay a “green premium” for homes with higher energy efficiency. A Domain report from May 2024 found that energy-efficient houses sold for 14.5% more, while efficient units fetched an 11.7% premium. In some areas, price differences were as high as 28%.

This willingness to pay more reflects a combination of long-term savings on running costs and the improved comfort offered by new builds.

Lender requirements

Lenders are increasingly factoring energy efficiency into their decisions, with many becoming reluctant to approve loans or provide coverage for homes with poor energy ratings.

Real Estate Institute of Australia director Jacob Caine told the Australian Financial Review, “We will see in the not-too-distant future almost mandatory requirements in lending from financial institutions for those properties that don’t meet minimum standards.”

He added that lenders may start adding clauses to contracts on home loans for older homes that agree to provide the finance only if upgrades are undertaken.

We are already seeing this trend, with the introduction of a federal government-led Clean Energy Finance Corporation fund which provides cheaper loans to homeowners wanting to make their homes more energy efficient. This mortgage option is currently available through Westpac and Bank Australia.

Government rebates and incentives

State governments are prioritising programs to upgrade existing housing stock. Financial incentives, such as rebates and grants, aim to help homeowners retrofit properties to meet modern efficiency standards.

For example, the ACT’s Home Energy Support program provides up to $5,000 in rebates to help with the cost of installing energy-efficient products. New South Wales offers the Energy Savings Scheme providing financial incentives to install energy-efficient equipment and appliances. Victoria’s Energy Upgrades offers discounts on energy-efficient products when replacing old, outdated appliances.

But, even with these programs, the cost of replacing or upgrading existing appliances or energy systems can add up, putting further upward pressure on existing home prices in comparison to new homes that come already fitted with energy-efficient systems.

Other incentives

For apartment developers, incentives are already in place through embedded energy networks. Providers like Energy Australia offer “free infrastructure” (such as hot water plants and equipment) to developers in exchange for residents sourcing their electricity through the embedded network. This lowers construction costs while making new apartments more appealing to buyers.

Running costs

To meet NatHERS requirements, new homes are often equipped with energy-efficient features including solar panels, water tanks and double-glazed windows. These help reduce running costs.

Roof and ceiling insulation can save up to 45% on heating and cooling

Wall insulation can save around 15% on heating and cooling

Sealing gaps around windows and doors can save 5-15% on heating and cooling

In contrast, older homes often require costly upgrades to achieve similar savings, such as installing insulation, replacing appliances or retrofitting windows. Without these improvements, owners of older homes may face higher utility costs that can deter buyers or renters.

Cooking and appliances also contribute significantly to a home’s running costs. As the image below shows, an average NSW household uses 40% of its energy on cooking and appliances.

New homes are typically fitted with energy-efficient appliances that meet current performance standards, such as induction cooktops, LED lighting and high-rated refrigerators and washing machines. These energy-efficient appliances consume far less power than their outdated counterparts in older homes, saving the homeowner or tenant on their running costs.

Future-proofing your investment

For investors, energy efficiency plays an important role in both capital appreciation and rental demand.

First, tenants are increasingly prioritising energy efficiency, with 72% of renters surveyed by PropTrack saying energy ratings help reduce their utility bills.

Second, in some locations like Victoria, landlords must already meet minimum energy standards for rental homes, and more regulations are under consultation. Retrofitting older homes to comply with these standards could be costly, further widening the price gap between new and existing homes.

Lenders’ interest rate discounts for energy-efficient homes and government incentives to upgrade older stock are clear signals that efficiency will play a central role in the market moving forward. For investors, newly built homes that meet NatHERS standards offer an opportunity to attract renters, save on running costs, and avoid costly retrofits.

CPC Lending Solutions is a property development and residential finance specialist. Whether you’re a developer needing funding for land, construction, or residual stock, or a buyer looking for the perfect mortgage, we’re here to help. Contact us at info@crowdpropertycapital.com.au or fill in this form.

https://crowdpropertycapital.com.au/wp-content/uploads/2024/12/Blog-image.jpg11781920dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2024-12-18 07:35:502024-12-18 07:35:50Energy efficiency: The growing gap between old and new investment properties

The New South Wales Building Commission is now under new leadership with the appointment of James Sherrard as building commissioner, succeeding David Chandler, who retired in August.

Sherrard’s appointment comes after the Commission’s establishment in December 2023, which elevated the role from NSW Fair Trading to an independent authority focused on enforcing building standards.

The NSW Building Commission’s mandate is to lift construction quality across the state, reducing defects in new builds through robust oversight. Its creation followed high-profile incidents, such as the Opal and Mascot Towers, which exposed structural issues and inconsistent enforcement of building standards in NSW’s apartment sector.

Its key functions include:

Managing disputes and complaints about building, renovation, trade or specialist trade work on residential and non-residential buildings

Inspections and compliance for building quality in residential construction

Licensing of tradespeople, design practitioners and certifiers

Policy development and reform of building laws in the state

Recent reforms to strengthen the building industry

Since its establishment, the NSW Building Commission has introduced several reforms aimed at raising standards and accountability in the construction industry. These reforms empower the Commission to take more decisive action in areas like inspection, licensing and product safety, all to safeguard consumers and improve construction quality across NSW.

Expanded inspection powers

One of the Commission’s significant changes is the authority to inspect properties under construction and mandate rectifications. Inspectors now have the power to enter any construction site, from apartment buildings to free-standing homes, to identify potential or existing defects.

The Commission can issue several orders, including:

Prohibition orders, blocking the issuance of occupation certificates or strata plan registrations

Stop work orders, halting a developer’s work if issues are identified

Building rectification orders, requiring defect remediation before work can continue

Anti-phoenixing measures

The Commission is also equipped with stronger anti-phoenixing powers, aimed at preventing developers from escaping financial obligations by dissolving and re-establishing companies. Under these new regulations, the Commission can reject, cancel or suspend licences for individuals involved in failed companies within the last 10 years.

Enhanced suspension powers

The Commission now has the authority to suspend certifiers, design practitioners and other key professionals if their ongoing work poses a serious risk, allowing for prompt intervention to safeguard public safety.

Strengthening building product safety

Starting in 2025, the Commission will introduce new requirements across the building product supply chain, impacting manufacturers, suppliers, importers and tradespeople.

These duties include ensuring compliance and sharing essential product information within the supply chain. The Commission also has the authority to issue warnings, enforce recalls and ban non-compliant products as necessary.

Cladding remediation

Finally, the Commission oversees Project Remediate, an initiative to replace flammable cladding on eligible apartment buildings, aiming to enhance safety through certified, fire-resistant materials.

CPC Lending Solutions is a property development and residential finance specialist. Whether you’re a developer needing funding for land, construction, or residual stock, or a buyer looking for the perfect mortgage, we’re here to help. Contact us at info@crowdpropertycapital.com.au or fill in this form.

https://crowdpropertycapital.com.au/wp-content/uploads/2024/11/NSW-gets-new-Building-Commissioner.jpg10801620dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2024-11-13 12:49:272024-11-13 12:49:27NSW gets new Building Commissioner

As interest rates have risen sharply over the last two years, the share of non-performing commercial real estate (CRE) loans at banks has increased, according to the Reserve Bank of Australia (RBA).

While this uptick may cause some concern, it’s worth noting that these levels remain low by historical standards. In fact, according to the RBA, “There continues to be little evidence of financial stress among owners of Australian CRE.”

Even in this challenging interest rate environment, now is a prime time to consider refinancing your loans in anticipation of potential interest rate cuts next year.

Interest rates forecast

According to the big four banks, the Australian Securities Exchange (ASX) and many other economists, the RBA is likely to start cutting rates early next year.

The global economic landscape is already trending downwards. Last month, the US Federal Reserve made its first interest rate cut. This followed several other big economies including the UK, Canada, China and Europe which have also begun their rate-cutting cycles.

And, because Australia typically follows a similar trend to these developed economies, it indicates we are likely nearing the end of the current cycle.

With rates set to ease and economists predicting cuts early next year, now is an ideal time to explore refinancing options. Waiting until the end of the year could leave you scrambling as the market slows during the holiday season, making it more difficult to explore loan options or secure approvals.

Fixed rates or not?

As you review your refinancing options, you’ll need to decide between a fixed-rate mortgage or a variable rate. Currently, some fixed rates are lower than variable rates, which may seem tempting. However, fixing your rate now could prevent you from benefiting when rates are cut further in 2025, as widely expected.

But, fixing rates now could lock you out of potential savings in the near future. If you fix your rate now and the RBA cuts rates multiple times in 2025 – as is expected – you could miss out on the lower payments that variable rates will offer next year.

Some borrowers have already seen potential savings with fixed rates, as some banks have begun lowering their rates (see table summarising lenders offering rates below 5.75%).

However, borrowers should keep in mind the longer-term benefits of not fixing rates.

For developers and investors, there’s a bigger picture. By choosing not to fix now, you’ll maintain the flexibility to adjust your strategy as rates continue to shift downwards, maximising your project’s profitability.

Private credit options

In the real estate sector, the private credit market is growing significantly. Private lenders who have matured over the last several years are actively looking for new sites and projects to finance. According to the RBA, as of July, around 11% of business lending and one-quarter of lending to small businesses was provided by non-bank lenders.

With traditional banks tightening their lending criteria, private lenders may fill that gap as an alternative source of funds for CRE.

Private lenders offer the flexibility and speed to capitalise on opportunities in a softening interest rate environment. Whether you are looking to refinance an existing project, purchase a new site or secure residual stock loans to buy time until rates fall, there are attractive options.

Now is the time to act

Whether you’re a borrower or an investor, now is the moment to explore your refinancing options. If you have an existing loan, refinancing could help you lock in lower interest rates and reduce your monthly repayments.

For developers, the current rate environment also presents an opportunity to invest in new projects. Market conditions are favourable for acquiring sites and starting developments, with the growing private credit market offering flexible and attractive funding options

Additionally, savvy developers can take advantage of residual stock loans, which offer temporary financial relief while planning their next move. These loans help bridge the gap until rates drop further, giving you more time to strategise.

CPC Lending Solutions is a property development and residential finance specialist. Whether you’re a developer needing funding for land, construction, or residual stock, or a buyer looking for the perfect mortgage, we’re here to help. Contact us at info@crowdpropertycapital.com.au or fill in this form.

https://crowdpropertycapital.com.au/wp-content/uploads/2024/10/How-to-capitalise-on-lower-rates-with-well-timed-refinancing.jpg10801618dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2024-10-14 09:02:172024-10-14 11:30:53Should I fix my new rate? How you can capitalise by refinancing in the current rate environment