As your apartment project moves towards completion with stock left to sell numerous lenders are now mandated to offer developers cost-effective residual stock funding.

This funding is usually required to repay construction debt and allow sufficient time to achieve sales of completed unsold stock. Residual stock loans can allow developers to move onto their next project without compromising sales prices.

Residual stock lending key information

First mortgage funding

Typically $2m to $30m loan value

Gearing to a maximum of 65% LVR against “in one line” valuation

Establishment Fees 1.5%

Rates 4.95%

Rapid decision and loan settlement

OUR PROCESSESS

CPC Development Lending Solutions secures market leading finance on your behalf – we get projects funded.

Working closely with our developer clients we are that new set of eyes that stress test your feasibility and project assumptions around revenue and costs.

We examine presales targets, project delivery team, transaction structure, funding request and timings. This allows your project to be presented professionally and takes it to the front of the queue leveraging off our strong non bank lending relationships.

https://crowdpropertycapital.com.au/wp-content/uploads/2019/07/New-Project-Completion.jpeg23363500CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2021-05-09 11:25:042021-05-31 12:52:32Apartment & Townhouse Residual Stock Funding - Free up your Capital

A registered first mortgage funding opportunity exists to fund a development project 11kms south of the Sydney CBD.

This opportunity is lead by highly experienced property development executives who are able to better assess risks and provide funding on loans with Loan To Value (LTV) ratios and Covenants that are reflective of the specific projects risk profile. The maximum LTV on this loan is 42% secured via first mortgage.

The developer has acquired the site for $26.5M in 2016 (100% equity funded). The total required facility of $11M is secured against the existing five lots. The maximum LVR is assumed to be 42% (subject to valuation).

The development is a 6,000m2 site yielding 168 apartments and is located 11km from the Sydney CBD. The site is 350m from the train station and 2km from Sydney Airport.

The exit strategy for this loan is the developer completing his current project in another suburb of Sydney. The developer has a solid track record of delivering apartment projects in Sydney (2012-2016 delivered 480 units over 5 projects, GDV $213M).

The minimum investment is $1.1M and interest is 10% paid monthly in arrears. This opportunity is open for a limited time only, further details are below.

INVESTMENT DETAILS*

Loan Facilty Type

Registered 1st Mortgage

Interest Rate (investor)

10% per annum

Total Loan

$11M

Minimum Investment

$1.1M

Loan Term

12 Month Facilty from settlement date

Max Loan to Value (LTV)

42% (subject to valuation)

Targeted Financial Close

Settlement occurred 1st September 2017

WHO CAN INVEST?

An investment of $1,100,000 or more by any Australian resident or non-resident.

Any business that is not considered a small business (less than 20 people)

Professional & sophisticated investors

An Australian financial services licensee

A body regulated by APRA include banks, building societies, credit unions, and life and general insurers.

A trustee of a superannuation fund

An approved deposit fund,

A pooled superannuation scheme

A listed entity, or a related body corporate of a listed entity.

To obtain further an Information Memorandum (IM) for this investment please contact dlovato@crowdpropertycapital.com.au or ph. 0434 932 634. *Refer to IM for additional information.

https://crowdpropertycapital.com.au/wp-content/uploads/2017/12/aerial-sydney-cbd.jpg636955CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2018-01-15 06:15:352020-01-08 15:55:211st Mortgage Debt Deal Southern Sydney Development Site

Marketplace lending provides a source of funds to consumers or businesses made possible via financial technology.

The ability to provide funding though non traditional channels allows businesses owners and consumers to access new forms of capital that weren’t accessible a few years ago.

So just how popular is marketplace lending? The growth of this alternative lending sector continues as more investors understand the risks and feel comfortable dealing with online marketplaces.

ASIC recently published its findings on the growth of online platforms, the regulator plays a major role, ASIC annually provides a marketplace lending survey.

This survey now in its 2nd year found:-

Total amount borrowed on lending platforms reached $300m last financial year

The number of retail investors using the platforms has increased from 2664 users to 6851 users in the last 12 months

The average reported default rate was 2.2%

Loan origination fees remains the primary source of revenue for marketplace lenders.

For further information on the survey and findings click HERE.

https://crowdpropertycapital.com.au/wp-content/uploads/2016/12/images-6.jpeg183275CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2017-12-11 04:42:452019-08-06 06:06:25Australian Marketplace Lending Surges to $300m in 2017

New research showing Australia has risen to become the second largest alternative finance market in the Asia Pacific sends a strong signal to the world about the underlying strength of Australia’s fintech and business environment.

Findings from a joint study by KPMG, the Cambridge Centre for Alternative Finance and the Australian Centre for Financial Studies, released today, reveals that Australia’s alternative finance market size grew by 53 per cent from 2015 to 2016 and has now reached US$609.6 million.

FinTech Australia CEO Danielle Szetho said the report’s findings showed how the Australian fintech industry – in areas such as invoice financing, balance sheet lending, peer-to-peer lending and crowdfunding – was servicing the nation’s strong economy and the needs of growing small and medium-sized businesses.

“The demand for our products and services is strong and our fintech lenders are rising to the challenge. This broad-based reports showcases the cumulative efforts of government and regulatory bodies like the Australian Securities and Investment Commission (ASIC) and Australian Prudential Regulation Authority (APRA) to support the accelerating momentum behind alternative finance in Australia,” Ms Szetho said.

At least 10 Chinese investors and developers who are yet to make their mark on Australia’s property scene are preparing to make an entry despite a recent slowdown in corporate activity driven by China’s upcoming National Congress and tougher foreign investment restrictions imposed by Chinese regulators.

New federal and state taxes on foreign buyers and tighter lending restrictions have also created negative sentiment for potential Chinese developers and investors. However, JLL’s head of China desk, Michael Zhang, said many Chinese real estate companies were still very serious about investing here.

“Australia continues to be a major investment destination for Chinese capital and many Chinese real estate companies are serious about having some footprint in Australia,” Mr Zhang said.

In a report called The Future of Chinese Residential Developers in Australia, JLL conducted analysis into the 10 largest residential developers yet to enter the Australian market.

Among the top 10 are Hong Kong-based Sun Hung Kai with a market capitalisation of $56 billion and Henderson Land, which recently paid a record $4 billion for a car park in Hong Kong. Other names include Evergrande and transportation business China Merchants Group.

“Some of the Chinese residential developers on this list are already showing interest in the Australian market or are involved in Australian industries outside of the residential real estate sector,” JLL senior analyst for residential research in Sydney and author of the report, Vince De Zoysa, said.

“We have already seen some of these firms enter Australia through other industries, in particular infrastructure. This allows them to establish a local presence in Australia in their core industry before moving up the risk and reward curve into residential development.”

A key driver for these developers will be the health of the foreign retail buyer market for new apartments in Australia. The federal budget changed the rules so that developers selling new multi-storey dwellings are now capped at vending 50 per cent of the total development to overseas buyers. Foreign owners will also start to incur a capital gains tax of 12.5 per cent when selling their main residential asset.

Interest from China remains high

“Despite increased taxes, tighter lending measures on development finance and limited availability of senior debt to overseas developers, the level of interest remains high for Chinese developers,” Mr Zhang said.

While Juwai.com has recently forecast Chinese buyers to spend $104.5 billion on global property this year, a significant fall from last year’s record high of $133.7 billion, Mr Zhang said that was not representative of a new wave of Chinese developers and investors.

“Australia continues to be a major investment destination for Chinese capital,” he said. “Australia’s average deal size is smaller than that of the US and the UK, which makes investing here accessible to investors of all sizes.

“Increasingly Chinese developers are seeking ready-to-go opportunities with existing DA or planning outcomes, thereby minimising planning risk and bringing clarity on project life cycle.”

Chinese corporate activity has slowed recently as a result of the upcoming 19th National Congress to be held in October. The tougher foreign investment restrictions imposed by Chinese regulators on $US1 billion-plus deals are still in place.

https://crowdpropertycapital.com.au/wp-content/uploads/2017/07/Chinese-Fav-Cities.jpg129391CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2017-07-13 21:03:492023-06-05 02:29:32The new Chinese investors about to make Australian foray

P2P lending is the practice of lending money to businesses through online services that match lenders with borrowers.

As we move into the second half of 2017 more property developers are having to turn to P2P lenders as their access to traditional forms of capital is tightening.

The major banks are extending less credit to property developers, as a result credit is drying up to many development companies who are turning to these P2P funding channels – usually at higher interest rates.

Investors now have a wide range of options to obtain higher yields via participating in these loans but sorting the out the good deals from the bad is not easy as these investments are unregulated and carry substantial risks.

We take a look at 5 key things you should know about P2P lending before making any investment decisions:

Don’t chase exceedingly high returns

If a debt offering is returning over 25% and is a “mezzanine style” deal chances are its extremely risky. A developer may have no options other than paying high rates like these over short periods but these deals are highly leveraged and need greater due diligence.

Bottom Line – Avoid deals that promise high rates of return, they are extremely risky and you may lose your capital.

Know your investment timeframe

P2P lending allows developers to use your funds to grow their business by providing capital to buy new sites or pay their bills on existing sites.

You generally won’t have the option of getting your funds back prior to the expiration of the agreed loan period. Most developers will need these funds for 12-24 months or longer until they complete their projects.

Be prepared for extended loan periods as projects encounter delays such as wet weather or underestimating the time to completion.

Bottom Line – Understand what project you are investing in and the agreed timeframes for your investment returns.

Investment Security

Just like the major banks, P2P investors should be looking at security in the underlying asset to protecting their investment.

Lending on a first mortgage basis is the safest way to ensure your investment is protected. If a developer defaults on your principle or interest repayments you still have the benefit of first mortgage security. This puts your investment in a strong position as you have underlying ownership of the land.

Bottom line – First Mortgage investment provides investment security.

Research the developer

Like the stock market, investors need to do some research. You need to understand the basics of a property market and drivers of economic development. How much of a track record does this developer (your borrower) really have?

Where is the project located? Is it close to new government infrastructure? Is there a need for housing, education, healthcare or retail services in that particular area?

Does the developer have a proven development team with delivery experience on completed projects? Who is their preferred builder? What is the builder’s experience?

Bottom Line – You should ask all these questions prior to investing.

Deal with reputable P2P lenders

Your best chance of a good initial (and repeat) experience in P2P lending is to do your research. The quality of the offerings (not quantity) is key. Online operators should have a local presence which is regulated by ASIC.

Bottom Line – There should always be someone you can talk to on any P2P website. Pick up the phone, make contact and get to know who you’re dealing with, you will soon find out if they know what they’re talking about.

About Crowd Property Capital: CPC is a modern property marketplace fueling a shift into the world that’s less dependent on the traditional incumbents and middle-men. For further information on P2P lending contact David Lovato on +61434932634 or visit https://crowdpropertycapital.com.au

https://crowdpropertycapital.com.au/wp-content/uploads/2016/12/images-6.jpeg183275CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2017-06-18 10:10:442019-08-06 06:01:46Peer 2 Peer (P2P) Lending - 5 Things you should know before investing

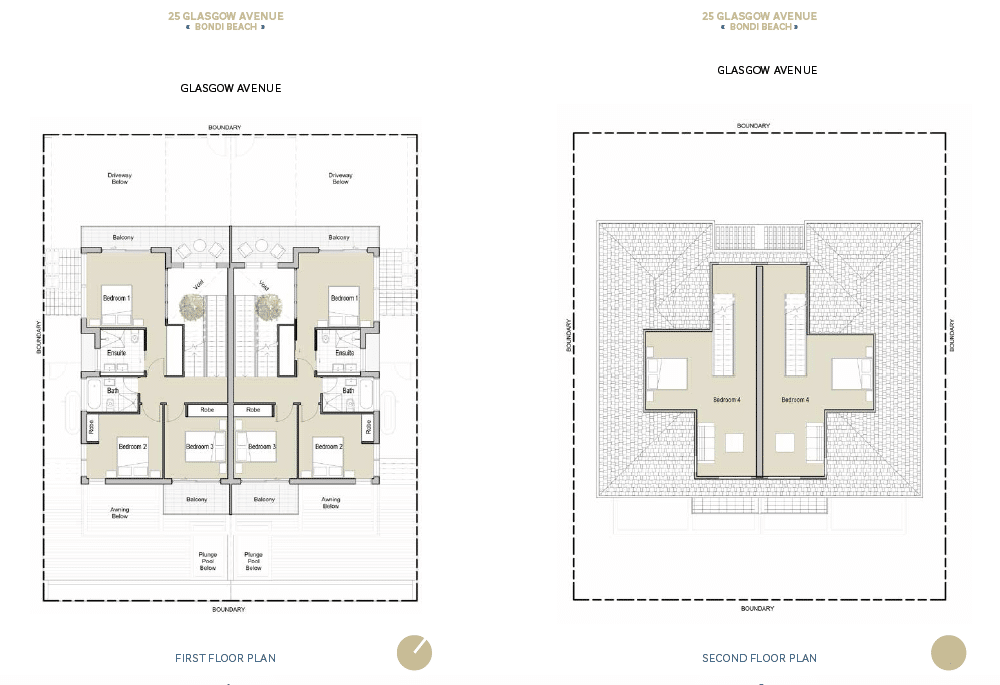

25 Glasgow Avenue is for sale by auction 8th April 2017

A development site with the opportunity to build two executive residences (STCA) is for sale by auction on 8th April 2017.

Located in the heart of Bondi Beach moments to the sand, surf, boutique shopping, and cafe precincts the property offers investors a solid value proposition.

Key investor information

Existing 3 Bedroom house on a 418m2 parcel with 18m frontage.

Raw development potential for two executive residences with car parking, extensive landscaping and plunge pool (STCA).

Strong rental yields post-acquisition, highly rentable existing 3 bed residence moments from the beach.

DA precedent for dual occupation design based on neighboring properties.

Whether your objective is to develop to sell both dwellings or live in one and sell the other this is a compelling investment opportunity.

The below information provides a concept design that has been produced in consideration of existing planning controls.

An artists Impression of the possible redevelopment of 25 Glasgow Ave Bondi Beach (STCA)

Basement and Ground Floor Design

The concept design allows off street parking for two cars, generous open plan living areas combined with a spacious outdoor rear deck area, plunge pool, and outdoor shower area. The front study could also be used as a 5th Bedroom.

The first floor and an attic level.

The first floor consists of three well-proportioned bedrooms, the master and rear bedroom have their own private balcony. Functional use of the roof has allowed a large 4th bedroom or teenage retreat in the attic space.

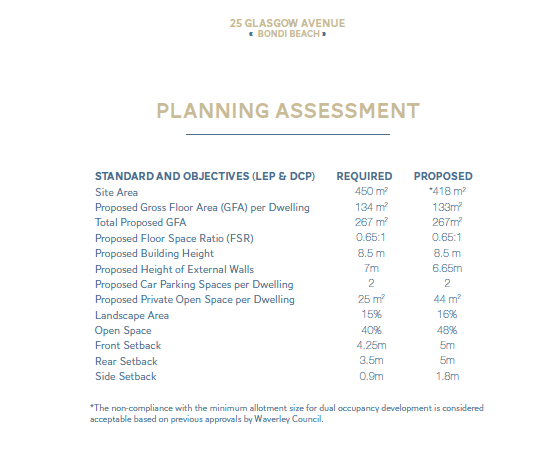

The above table summarises the proposed design based on the current planning controls of Waverley Council.

For further due diligence information on this property:

Disclaimer: No enquiries have been made with Waverley Council regarding the suitability or acceptance of this or any potential Development Approval. While much care has been taken to ensure that the data presented is accurate investors should make their own enquiries. This information should not be relied upon for valuation purposes.

Existing property at 25 Glasgow Ave Bondi Beach

https://crowdpropertycapital.com.au/wp-content/uploads/2017/03/Print_25-Glasgow-Avenue-Bondi-Drone-8.jpg27043605CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2017-03-19 10:27:252019-08-06 05:53:0725 Glasgow Avenue Bondi Beach - Unique Raw Development Site Opportunity

March 2017 Written By: Andrew Medal – Entreprener.com

Crowdfunding is rearranging the way that entrepreneurs finance their creative endeavors, whether they’re artists or engineers. From bringing startups a needed capital boost to getting students money to go to college, crowdfunding seems to be creating opportunity in almost everything.

More and more investors are noticing the clear-cut advantages offered by crowdfunding platforms, and it’s no surprise that they are rushing to claim their piece of the pie. In 2015, it was estimated that more than $34 billion was put into crowdfunding efforts.

At its current growth rate, the crowdfunding industry is multiplying in size every year. It’s trickling into several types of funding models (donation, equity and lending) and an array of industries (education, medical care and corporate finance). Whether willing or not, the majority of industry markets will be facing a major disruption in how capital is moved throughout the economy.

Here are the top three industries the crowdfunding sphere is set to disrupt and why:

1. Corporate finance: From software to farm equipment

Each year, U.S. companies invest in leased tools that range from software to construction equipment. As crowdfunding persists in its growth, the companies who lease utilities as a part of their businesses will have to engage with the crowdfunding sphere. The companies that embrace crowdfunding early will rake in the benefits of accessing small businesses that flock to it as a tool.

Large finance organizations can use it as a catalyst for gaining small businesses who seek to harness leased products that are tailored to them specifically. What’s more, the lower cost credit of the products they offer will appeal more to businesses that pay sky-high APRs.

For leaseholders of larger equipment, crowdfunding platforms will allow leaseholders such as farmers to finance crops and equipment from other farmers and associates. It’s in this way that their crowdfunding platforms will provide communities with better access financing.

2. Real estate: From housing to business establishments

For the real estate market, crowdfunding presents a huge solution. Before crowdfunding, closing an actual real-estate deal required back and forth passing and signing of documents among lawyers. Beyond being slow, the process often added up to thousands of dollars in legal fees. Crowdfunding allows businesses of all sizes to bypass the monotonous process and dodge expenses. What’s more, real-estate crowdfunding allows potential investors access to a wider array of deals.

Mark Suleman, the founder of real estate crowdfunding platform Macrocrowd, sees the benefits of this type of access firsthand. “I always hear from clients about how they struggled to access the right people and resources while looking for real estate investments abroad,” he explains. “But by getting on board with crowdfunding, though I can’t speak for other platforms, they’re able to access quality investments into institutional real estate — globally.”

It’s not just accessibility that’s grabbing the attention of venture capital dollars. Today’s internet-reliant consumer is well beyond acquainted with making investments online. Users are becoming more and more comfortable with putting their money into crowdfunded sites. For real estate businesses who get their hands into crowdfunding, this means access to a whole new crowd of their own.

3. Consumer lending: Cars and home appliances

While banks have backed away from lending consumer and small business with credit, peer-to-peer crowdfunding platforms are leaning in. As big banks begin to take themselves out of the equation, institutional and professional investors will begin to swoop in and sign up for them too.

For financial institutions, this means learning to leverage a crowd’s interest to inform their lending offers. As the trend continues, new crowdfunding platforms will pop up to cater to specific lending verticals. Imagine a crowdfunding space where consumers can get loans for anything related to transportation or kitchen appliances. In this way, brands will be able to save on financing costs while gaining on capital returns.

https://crowdpropertycapital.com.au/wp-content/uploads/2017/02/Crowd-Funding.jpg193262CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2017-02-25 19:28:182019-08-06 06:04:363 Industries Being Disrupted by Crowdfunding

Knight Frank have just released a report into emerging trends of Chinese developers in Australia, the report shows statistically an insatiable appetite for site acquisition throughout the country. This long term trend is set to continue and it’s impacting local developers as they become the under-bidders and miss out on new sites.

The following are key takeaways from the report:

Chinese developers are buying larger sites, average dwellings per site in 2016 = 502 (versus 2012 = 103);

Chinese site acquisition represent a massive 38% of all direct residential sites in Australia (versus 2% in 2012)

Chinese developers are interested in larger sites and are diversifying from apartment sites into house and land product.

These statistics underpin the strength of demand for Australian residential assets. This interest driven by China is a net positive for our region as it ultimately results in increased economic activity which in turn creates jobs.

https://crowdpropertycapital.com.au/wp-content/uploads/2017/02/Year-of-the-Rooster.jpg225225CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2017-02-02 20:08:512023-06-05 02:28:27The Rise of Chinese Developers in Australia

Airbnb owns no real estate…..Uber owns no vehicles.

Ten years ago I bet you had never heard of Airbnb or Uber, in fact even a few years ago these companies weren’t household names. Today they are getting bigger and bigger in the economic world of the “sharing economy”.

Airbnb and Uber are US tech start-ups that chose their industry – Airbnb (hospitality) and Uber (transport) these startup disruptors are today worth $30B and $68B respectively.

These industries have been shaken up to the detriment of the existing incumbents and they are not going away. They’ve upset a lot of people along the way, leaving other competitors fighting to remain profitable and regulators playing catch up.

So why are they thriving?

People now see a clear benefit in using financial technology services over outdated old world businesses, the last 5 years has seen the economic landscape reshaped to the point of no return.

WTF is happening?

What’s happening is a massive economic shift on a global scale, it’s a reinvention of how we transact and how much we pay for a service.

The invention of an internet based scalable service on an inefficient industry has been made possible by financial technology or fintech. It’s the start of what I call the smarter economy.

This global change is transforming not just transport and hospitality but also property and finance, the banks are in the fintech cross hairs scrambling to remain profitable and relevant.

Our Banking System – Get Set for Disruption

In the smarter economy, banks become less relevant as consumers (both businesses and individuals) realise the Uber effect -smarter and cheaper ways to borrow, invest, research and transact.

Imagine a massive 150-year-old organisation with hundreds of shopfront locations, thousands of staff, old and clunky internal processes and life long employees on huge salaries. Sound expensive? It is expensive….this is your typical incumbent bricks and mortar bank still making huge year on year profits.

Users of banks are becoming smarter and empowered through technology. Do we need to visit a bank to transact? No. Do people want a better deal from their bank? Yes. Do people have loyalty to their bank? No.

So where will we be in 10 or 20 years in the smarter sharing economy? I’m not 100% sure but I can guarantee many of the traditional business models will no longer be around and although many new businesses will fail you can bet the likes of AirBnB and Uber will be thriving.

Crowd Property Capital is a non-bank lender that effectively cuts out the middle-men in business loan transactions. Put simply an investor (business or individual) who has funds to loan can provide a borrower with these funds on agreed terms. The lender receives a rate between 8-12% pa and the borrower gets access to funds faster. Investments are available on a wholesale basis to local and international sophisticated investors with a minimum investment of $500,000 AUD. For more information visit www.crowdpropertycapital.com.au

https://crowdpropertycapital.com.au/wp-content/uploads/2017/01/AirBnb2.png183275CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2017-01-26 02:12:242023-06-05 02:16:57WTF is Happening? How Airbnb and Uber are Reinventing Economics