Written by David Lovato – CPC Development Lending Solutions

There are many factors a property developer needs to consider when starting a new development.

For example, if you want to finance a new development, you’d probably need to:

* Pre-sell the properties

* Apply for bridging loans

* Apply for specialised property loans

* Apply for personal loans

When assessing these applications, lenders could consider all or one of the following:

* You and your business’s credit history

* You and your business’s track record if you’ve developed properties before

* The business plan and viability of the project

Consulting a development finance specialist could help you:

* Make the right finance choices

* Get your development financed sooner by helping you with your application and business plan

* Potentially save you money by getting you better interest rates

___

Need development finance? CPC Development Lending Solutions can help you get your next project funded. To confidentially discuss your options, contact David Lovato on +61 434 932 634 or info@crowdpropertycapital.com.au

https://crowdpropertycapital.com.au/wp-content/uploads/2023/02/Cronulla-Internal.jpg7201094dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2023-02-21 06:46:492023-06-05 02:28:45What developers should consider when starting a new development

Written by David Lovato – CPC Development Lending Solutions

As any developer knows, finding the right finance is critical to your project getting off the ground. But getting all the funds in place can be a time-consuming and frustrating process. With the RBA starting the rate rising cycle in May cheap commercial loans via bank funding are becoming more expensive and less attractive.

Non-bank lenders have taken a growing market share since the GFC as bank regulations tightened over the last decade. This has lead to more competition which is great news for you, because borrowing through non-bank lenders offers some big benefits. Interestingly as bank lending tightened, non-bank lending loosened leading to a wild west mentality. Not all lenders are reputable, there are many pitfalls but doing deals with the best non-banks can be rewarding and will help you grow your business.

The advantages of non-bank finance

Non-bank lenders are typically privately owned and operated. So they can offer credit with fewer strings attached than traditional banks, such as:

Lower pre-sales requirements to start construction

Lower equity requirements, freeing up cash to drive your future development pipeline

What’s more, you get to deal with funders who understand property partnerships, repeat business and an entrepreneurial mindset. So they will generally approve or decline your application within days (not weeks or months like the banks).

Non-bank lenders also generally adopt a whole-of-business approach: they focus on the bigger relationship rather than the individual transaction. So If things don’t go to plan, you can work with them to ensure a win-win outcome.

What’s the cost of a non-bank loan?

Lenders charge various upfront and ongoing loan fees, so the cost of a loan isn’t just about the interest rate. The devil is in the detail, because steep charges and loan fees can eat into your profits, making your project unviable.

Three factors determine non-bank rates and fees:

The loan’s risk profile

The project’s profitability

The borrower’s financial strength

A word of warning. Some lenders are deliberately vague about the applicable fees and charges, leaving you to discover them for yourself after you’ve committed to the loan.

For example, many loans come with a discounted interest rate that reverts to a higher rate if the loan terms are altered without mutual agreement during the loan term.

So it’s vital you’re clear on all applicable fees, charges and conditions before you apply. A specialist development finance broker such as CPC can help with this.

Five common mistakes to avoid

CPC has heard countless horror stories of developers trying to save money by arranging finance themselves, rather than through a specialist finance broker.

This usually ends badly.

That’s because these developers often end up making mistakes such as:

Falling for too-good-to-be-true deals

Some non-bank lenders lure borrowers by promising them fees and interest rates that seem too good to be true. Sadly, these lowball offers are generally scams.

Getting overcharged

You should also be wary of lenders that charge large upfront fees or seek caveats on your property to secure their fees before getting started on due diligence. Reputable lenders charge only a nominal upfront fee (to make sure the borrower is serious), which then gets refunded at settlement.

Signing up for punitive penalty clauses

Watch out for clauses in offer letters or loan agreements that impose heavy penalties for breaches of loan terms.

Committing to long minimum interest periods

Be careful of loans that require you to pay interest for a minimum number of months, as you might end up being penalised for paying down debt early.

Working with fake lenders

Some unscrupulous brokers portray themselves as lenders and charge large upfront commitment fees. Once you’ve paid, they find excuses not to write the deal.

Why work with CPC?

Even the most experienced property developer finds it hard to choose the right non-bank lender and loan product. That’s because there are many lenders on the market, each offering different loan products, borrowing criteria, interest rates, and fees and charges. But you need to get it right, because you don’t want to make an expensive mistake that prevents your project from breaking ground.

That’s where CPC comes in.

We’re a specialist development finance broker, and have been arranging funding for our clients since 2014.

We work only with well-established, reputable non-bank lenders that have:

Operated through different market cycles

Got a strong track record for managing loans from beginning to end

So you can be confident the lender we find for you will have:

Sufficient funds available

Demonstrated cashflow management

A loyal, long-term investor base

CPC unashamedly charges a nominal upfront fee. This ensures we can dedicate time to your project, so we can better understand you and your objectives.

We can then match you to the right lenders, presenting your project in the best light so they are keen to win your business.

Need development finance? CPC Development Lending Solutions can help you get your next project funded. To confidentially discuss your options, contact David Lovato on +61 434 932 634 or info@crowdpropertycapital.com.au

https://crowdpropertycapital.com.au/wp-content/uploads/2022/05/qtq80-pG0uL0.jpeg14402190dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2022-05-13 02:38:122023-06-05 02:29:27The Pros and Cons of Non-Bank Lending Explained

Written by David Lovato – CPC Development Lending Solutions

Have you ever wondered what might happen if your builder went bust halfway through your project?

I have first-hand experience of this problem.

Back in 2009, during the GFC, I was a young project manager working for an ASX-listed developer, when a builder that was doing three of our projects entered administration. All our sites got locked overnight. It turned out the builder owed $30 million to their creditors. We were shut out of our projects for six months, until we were able to legally take back possession of the sites and engage a new builder. It was a costly lesson.

So the thing that happened to my employer all those years ago might happen to you too.

How to protect yourself from financial risk

Don’t choose a builder based solely on a Google search. There’s too much money at stake for that. Instead, do thorough due diligence.

Here are three steps you should take to minimise your risk:

Check their financials

It’s perfectly legitimate to ask a builder to provide their most recent tax return and a consolidated cashflow forecast. Be wary of builders that are reluctant to provide this information. You want to understand who their other clients are and whether they’re properly resourced to manage multiple projects. You also want to find out how much revenue they’ve forecast for the next two years, because, with some builders, their cashflow might be destroyed if even one client refused to make a progress payment.

Check their legals

It’s important to understand your builder’s company structure and class of licence. Be wary of builders that set up shelf or subsidiary companies for their building contracts. You should always understand who the directors are, and if they’ve had any insurance or legal claims against them, whether with this company or another one. Also, take the time to review the individual licence details of the nominated supervisor to make sure that person hasn’t had any historical compliance issues.

Do a credit check

Engage a credit and risk assessment firm like Newpoint Advisory or Dun & Bradstreet to do a background check on any builder you’re thinking about engaging.

Don’t forget to do these background checks as well

There’s more to due diligence than just doing finance and legal checks.

When you research builders for development projects, you should also do these three things:

Check for relevant experience

Of course, you want to choose an experienced builder. But you also need to make sure your builder is experienced in the specific project you’re planning. For example, if you’re going to develop apartments, don’t engage a builder that only has house experience. Choosing a specialist will mean your builder will understand the building codes and design issues relevant to your type of project, and will also know subcontractors with relevant experience.

Visit previous projects

Any builder you talk to will tell you how great they are (and will probably have some nice-looking photos too). But you wouldn’t be conducting proper due diligence if you took their word for it. So take the time to visit some of their finished projects. Also, speak to building and strata managers to find out how responsive they’ve been when residents have moved in and they’ve been asked to fix any problems that have cropped up. That will tell you how committed they are to delivering quality work and maintaining their reputation.

Talk to other clients

Ask your builder to provide contact details for two or three other clients. When you speak to those other clients, ask them what sort of quality the builder delivered, how they managed the project, what their service was like and how their subcontractors acted.

CPC Development Lending Solutions can help you get your next project funded. To confidentially discuss your options, contact David Lovato on +61 434 932 634 or info@crowdpropertycapital.com.au.

https://crowdpropertycapital.com.au/wp-content/uploads/2022/04/CPC-Builders-Insolvent-1.jpg360643dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2022-04-25 06:34:552023-06-05 02:28:39How to choose the right builder for your next commercial development

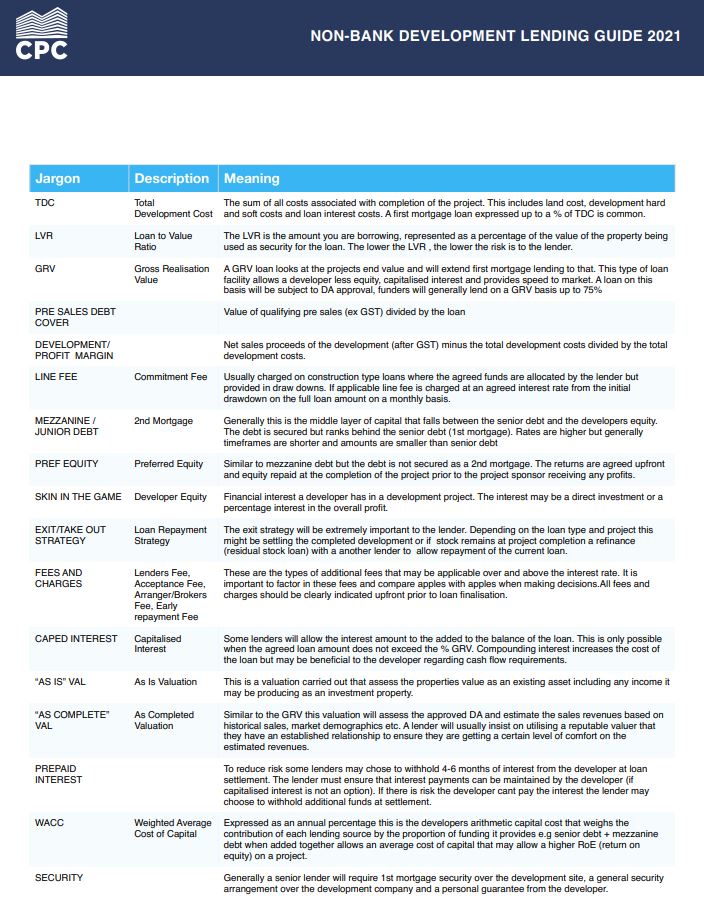

National “Drop the Jargon Day” for the healthcare industry is on Tuesday 20th October so here’s some meanings around jargon that exist within the non-bank lending space.

Working in development finance you come across many personalities and a lot of ego’s. Eliminating jargon actually makes you appear more intelligent than less. For now we need to live with jargon so here’s a cheat sheet of terms used in our industry.

The bottom line is no one knows everything so when someone tries to bamboozle you with industry jargon ask them to explain what they mean.

Download the CPC Lending Guide by clicking below for more insights into the non-bank lending space for development projects.

CPC Development Lending Solutions secures market leading finance on behalf of developers – we get projects funded.

Working closely with our clients we are that new set of eyes that stress test your feasibility and project assumptions around revenue and costs.

We examine presales targets, project delivery team, transaction structure, funding request and timings. This allows your project to be presented professionally and takes it to the front of the queue leveraging off our strong non-bank lending relationships.

Engaging with CPC allows you to focus on managing your project and driving your consultant team. If you are looking to break ground in 2022 get in touch now. Its never too early.

For more information about CPC Development Lending Solutions check out our FAQ page

To confidentially discuss your bespoke funding solution contact us today on email info@crowdpropertycapital.com.au or phone +61 434 932 634

These are unprecedented times with no one able to predict the future, CPC has summarised 5 of the key metrics private lenders are currently focusing on to ensure they are investing in the right projects suitable to the current climate. To ensure you can secure funding for your next project look at these metrics closely and see how your project stacks up.

Metric 1 – DEVELOPER EXPERIENCE

Private lenders want to partner with experienced developers who have cut their teeth on past projects and learnt from their mistakes and experience. They are ready to back project sponsors who can demonstrate its not their first project and have runs on the board.

Metric 2 – PROJECT LOCATION

Middle ring suburbs with median price points, close to the CBD, excellent existing infrastructure (not promised). With foreign buyers are temporarily out of the local market and immigration suspended there is a renewed focus on a local catchment and established suburbs that have had recent gentrification and infrastructure investment. Locations that appeal to families, downsizers, retirees are strongly preferred by lenders.

Metric 3 – PROJECT SIZE

Lenders are spreading risk by project diversification. A loan book with more projects at a lower investment value per project is much more attractive than a loan book with the same FUM made up of one or two large projects. Smaller boutique style projects make a lot of sense to lenders, less stock to shift, more competitive build environment and generally less project risk. If your project is from 2 to 15 dwellings you are more likely to get funding and your project started sooner.

Metric 4 – DEVELOPER EQUITY

Key loan to value ratios have shifted post COVID-19. Senior debt secured by 1st mortgage remains the focus for quality stable lenders. Generally lenders will require developers to put more equity into projects upfront, GRV around 65-70% is current senior. Mezz is available but is still expensive. Developers also need to ensure they are not to heavily reliant on cash flow from other project completions.

Metric 5 – PRE SALES

Lenders will typically favour projects that have exiting pre sales purely due to the potential impact of COVID-19 on property prices. Having presales also proves to a lender you have a sales process in place that is delivering in these challenging times. Sales revenue remains one of the biggest risks to all projects moving forward.

OUR PROCESSESS

CPC Development Lending Solutions secures market leading finance on your behalf – we get projects funded.

Working closely with our developer clients we are that new set of eyes that stress test your feasibility and project assumptions around revenue and costs.

We examine presales targets, project delivery team, transaction structure, funding request and timings. This allows your project to be presented professionally and takes it to the front of the queue leveraging off our strong non bank lending relationships.

Engaging CPC allows you to focus on managing your project and driving your consultant team. If you are looking to break ground in 2022 get in touch now. Its never too early.

For more information about CPC Development Lending Solutions check out our FAQ page

To confidentially discuss your bespoke funding solution contact us today on email info@crowdpropertycapital.com.au or phone +61 434 932 634

https://crowdpropertycapital.com.au/wp-content/uploads/2020/04/Covid-19-Australia.jpg9881536CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2021-08-16 00:51:332023-06-05 02:08:175 Key Metrics Private Lenders are focused on during the COVID Pandemic

I always get asked by developers when should I start seeking construction funding for my project? Every time my answer is – As early as possible!

Its never too early to be seeking finance in this current climate and this is why.

Our industry like many others is going thru a COVID related shift. Development professionals (architects, engineers, valuers, QS, lenders) are choosing to work more remotely from home, taking on more work and perhaps not working as efficiently as before. This remote working shift may ultimately become more streamlined as technology and management mindsets change – but we are not there yet.

Currently property industry businesses are finding it hard to onboard and employ additional staff. As demand increases processes and reports are taking longer to finalise. For example lending valuation report timeframes have recently doubled from normally 3-4 weeks to now 6-8 weeks. Some companies are refusing new work as they struggle to keep up.

The bottom line is to expect longer lead-in times to get your project commenced. Try to de-risk all aspects of your project that you have control over. The earlier you start the important process of securing project funding the better off you’ll be. You might not have your DA approved, appointed a selling agent or engaged your preferred builder – it doesn’t matter, its never too early.

CPC Development Lending Solutions secures market leading finance on your behalf – we get projects funded.

Working closely with our developer clients we are that new set of eyes that stress test your feasibility and project assumptions around revenue and costs.

We examine presales targets, project delivery team, transaction structure, funding request and timings. This allows your project to be presented professionally and takes it to the front of the queue leveraging off our strong non bank lending relationships.

Engaging CPC allows you to focus on managing your project and driving your consultant team. If you are looking to break ground in 2022 get in touch now. Its never too early.

For more information about CPC Development Lending Solutions check out our FAQ page

https://crowdpropertycapital.com.au/wp-content/uploads/2021/05/qtq80-qvt17k.jpeg8371254dlovatohttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngdlovato2021-05-31 11:24:242023-06-05 02:11:23Breaking Ground in 2022? Start your development funding journey now!

As your apartment project moves towards completion with stock left to sell numerous lenders are now mandated to offer developers cost-effective residual stock funding.

This funding is usually required to repay construction debt and allow sufficient time to achieve sales of completed unsold stock. Residual stock loans can allow developers to move onto their next project without compromising sales prices.

Residual stock lending key information

First mortgage funding

Typically $2m to $30m loan value

Gearing to a maximum of 65% LVR against “in one line” valuation

Establishment Fees 1.5%

Rates 4.95%

Rapid decision and loan settlement

OUR PROCESSESS

CPC Development Lending Solutions secures market leading finance on your behalf – we get projects funded.

Working closely with our developer clients we are that new set of eyes that stress test your feasibility and project assumptions around revenue and costs.

We examine presales targets, project delivery team, transaction structure, funding request and timings. This allows your project to be presented professionally and takes it to the front of the queue leveraging off our strong non bank lending relationships.

https://crowdpropertycapital.com.au/wp-content/uploads/2019/07/New-Project-Completion.jpeg23363500CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2021-05-09 11:25:042021-05-31 12:52:32Apartment & Townhouse Residual Stock Funding - Free up your Capital

The COVID-19 pandemic is reshaping economies around the globe with the local lending environment for development projects changing rapidly since March.

The property industry has already seen major impacts with lenders passing on riskier projects resulting in a substantial reduction in deal flow. One of the key changes over the last few weeks is the reduction in Loan to Value Ratios (LVR’s).

Lenders are requiring more equity from developers to protect their loan investment. We have seen a general reduction in risk/gearing with increased pricing. There are genuine post COVID deals being done now giving us and our clients the benefit of real time risk and pricing benchmarks.

If you are in the market for project funding there are options available as long as your project generally sits within the following criteria :-

First mortgage funding only

DA approved projects preferred with minimal planing risk

Experienced project sponsors with access to additional equity

Loan size $3m to $10m max

Gearing to a maximum of 55% LVR against GRV

Postcodes with no actual (or perceived future) oversupply

Purchaser demographic – local owner occupier focused, not reliant on investors

Generally 15 month max loan period

Zero pre-sales still available for smaller projects (2 – 10 dwellings)

Projects that sit outside of the above criteria may find it challenging in the current climate to secure funding. Some of our lenders at the moment are carrying out internal valuations as they reduce reliance on external valuer reports instead relying on their in house lending expertise and committees loan decision making.

CPC has a solid network of reliable private lenders who understand risk and property cycles – they are open for business and adjusting their lending criteria to strengthen their loan book in this current market cycle. The private lending market for developers remains active in pockets and generally excited by opportunities this dislocation is providing.

To confidentially discuss your bespoke funding solution contact us today on email info@crowdpropertycapital.com.au or phone +61 434 932 634

https://crowdpropertycapital.com.au/wp-content/uploads/2020/04/Approved-Rejected.jpg393620CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2020-04-22 23:14:042020-06-07 06:29:32Lower LVR's - The New Normal for Developers

A registered first mortgage funding opportunity exists to fund a development project 11kms south of the Sydney CBD.

This opportunity is lead by highly experienced property development executives who are able to better assess risks and provide funding on loans with Loan To Value (LTV) ratios and Covenants that are reflective of the specific projects risk profile. The maximum LTV on this loan is 42% secured via first mortgage.

The developer has acquired the site for $26.5M in 2016 (100% equity funded). The total required facility of $11M is secured against the existing five lots. The maximum LVR is assumed to be 42% (subject to valuation).

The development is a 6,000m2 site yielding 168 apartments and is located 11km from the Sydney CBD. The site is 350m from the train station and 2km from Sydney Airport.

The exit strategy for this loan is the developer completing his current project in another suburb of Sydney. The developer has a solid track record of delivering apartment projects in Sydney (2012-2016 delivered 480 units over 5 projects, GDV $213M).

The minimum investment is $1.1M and interest is 10% paid monthly in arrears. This opportunity is open for a limited time only, further details are below.

INVESTMENT DETAILS*

Loan Facilty Type

Registered 1st Mortgage

Interest Rate (investor)

10% per annum

Total Loan

$11M

Minimum Investment

$1.1M

Loan Term

12 Month Facilty from settlement date

Max Loan to Value (LTV)

42% (subject to valuation)

Targeted Financial Close

Settlement occurred 1st September 2017

WHO CAN INVEST?

An investment of $1,100,000 or more by any Australian resident or non-resident.

Any business that is not considered a small business (less than 20 people)

Professional & sophisticated investors

An Australian financial services licensee

A body regulated by APRA include banks, building societies, credit unions, and life and general insurers.

A trustee of a superannuation fund

An approved deposit fund,

A pooled superannuation scheme

A listed entity, or a related body corporate of a listed entity.

To obtain further an Information Memorandum (IM) for this investment please contact dlovato@crowdpropertycapital.com.au or ph. 0434 932 634. *Refer to IM for additional information.

https://crowdpropertycapital.com.au/wp-content/uploads/2017/12/aerial-sydney-cbd.jpg636955CPC adminhttps://crowdpropertycapital.com.au/wp-content/uploads/2024/07/CPC-LOGO_Landscape-Updated-Tag-OL-WHITE.pngCPC admin2018-01-15 06:15:352020-01-08 15:55:211st Mortgage Debt Deal Southern Sydney Development Site

New research showing Australia has risen to become the second largest alternative finance market in the Asia Pacific sends a strong signal to the world about the underlying strength of Australia’s fintech and business environment.

Findings from a joint study by KPMG, the Cambridge Centre for Alternative Finance and the Australian Centre for Financial Studies, released today, reveals that Australia’s alternative finance market size grew by 53 per cent from 2015 to 2016 and has now reached US$609.6 million.

FinTech Australia CEO Danielle Szetho said the report’s findings showed how the Australian fintech industry – in areas such as invoice financing, balance sheet lending, peer-to-peer lending and crowdfunding – was servicing the nation’s strong economy and the needs of growing small and medium-sized businesses.

“The demand for our products and services is strong and our fintech lenders are rising to the challenge. This broad-based reports showcases the cumulative efforts of government and regulatory bodies like the Australian Securities and Investment Commission (ASIC) and Australian Prudential Regulation Authority (APRA) to support the accelerating momentum behind alternative finance in Australia,” Ms Szetho said.